YTL: why so stingy? (2)

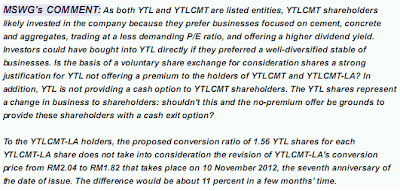

MSWG wrote about the same issue in in their newsletter January 12, 2012:

In the mean time, OSK has issued their independent advice. With the risk of repeating myself, it is not very good, I miss any critical remarks whatsoever about the issues at hand.

Those issues are:

YTL Corp's shares are more liquid, however, OSK fails to notice that 97% of the shareho…

Keep reading with a 7-day free trial

Subscribe to Asia Sentinel to keep reading this post and get 7 days of free access to the full post archives.