Covid-19 Drives Huge Jobless Bounce, Wrecks Consumption

Global downturn all but certain

By: Toh Han Shih

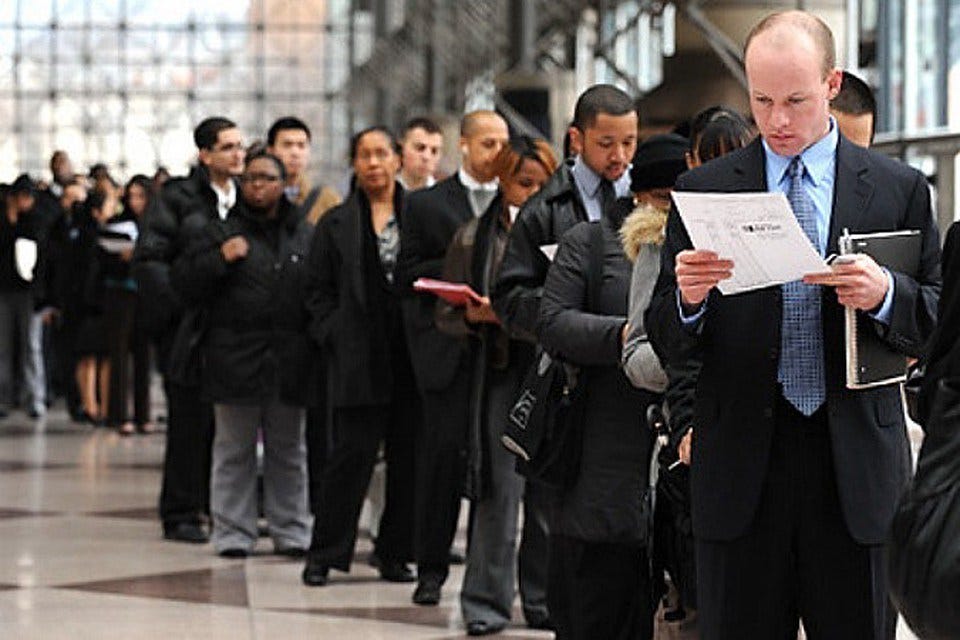

With a global recession all but certain, the Covid-19 pandemic is expected to jack up world unemployment to its highest level in recorded history and batter global consumption, according to a wide and almost-unanimous range of analysts, with Moody’s Investor Service, for instance, warning on March 25 that the virus “will cause an unpre…

Keep reading with a 7-day free trial

Subscribe to Asia Sentinel to keep reading this post and get 7 days of free access to the full post archives.