Maybulk: before and after POSH

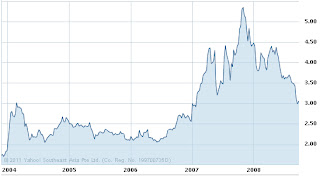

This is the share price chart until the announcement of POSH:

It reached a high of RM 5.40, it had come down since then due to the global economic outlook. Also there were worries about oversupply for tankers and bulk carriers. On the other hand, Maybulk would go into the recession with more than RM 1,400,000,000 in cash and short term deposits (Septembe…

Keep reading with a 7-day free trial

Subscribe to Asia Sentinel to keep reading this post and get 7 days of free access to the full post archives.