Bursa should ban the use of DCF valuations

The circular can be found here:

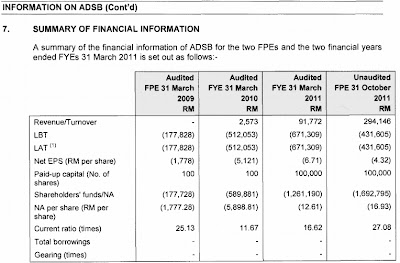

The financials of ADSB are as follows:

The numbers do not look exactly attractive, cumulative revenue over the first 3 years of operating were not even RM 100K. Due to the history of loss making the shareholders' f…

Keep reading with a 7-day free trial

Subscribe to Asia Sentinel to keep reading this post and get 7 days of free access to the full post archives.